How Will You Hatch Your Nest EGG?

We’ve launched a process to help you structure a plan based on three integrated objectives: generating income for the rest of your life, preparing for potential healthcare needs and creating a legacy.

Learn more about the Nest EGG Analysis.

Taking Stock of Your Resources

Here’s the greatest challenge to retirement planning: many will spend 30 or more years in this stage of their lives. To complicate matters, Americans often underestimate their own life expectancy; sometimes by five years or more.

With increased life expectancy, there is a clear need to expand traditional retirement planning to consider changes that go beyond tangible wealth.

The aim of the Nest EGG Analysis is to help you revisit and prioritize your goals, allowing you to make informed decisions now and into the future on issues which sometimes can be difficult. The dilemma faced by many is structuring an investment portfolio to meet a reasonable set of retirement goals on one hand and a proper balance of risk on the other.

The planning starts with taking stock of your resources.

Mitigating Risks

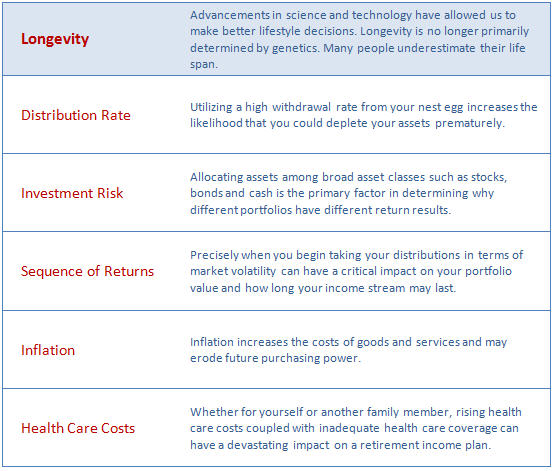

In our analysis, the common thread that links most of the major risks together is longevity. Living longer means you will incur more healthcare expenses; inflation will have a bigger stake in the planning process; the higher the distribution rate you take, the less likely it will last a lifetime; thus, if longevity should be on your side, the risk of outliving your resources should be addressed.

Risks in Retirement

By scrutinizing these risks, and the other risks not directly linked to your longevity (sequence of returns and investment risk), we provide a comprehensive assessment of your wealth, health and legacy — in other words the stage is set for longevity planning.

Income Distribution Strategies

Income distribution is an entirely different proposition than accumulating your nest egg. When considering best practices for income distribution there are three dominant approaches: the Time Segmented Allocation, Systematic Withdrawal Method and the Monthly Paycheck,

Below we highlight the Time Segmented Allocation, because in our opinion it does a good job at addressing some of the inherent risks we have identified.

Generally speaking, retirement investors who have not made a plan are most susceptible to reacting emotionally to market volatility. And for those with a plan, problems can arise when markets go to extremes and investors give in to powerful emotions.

One noteworthy strategy to combat against making emotional decisions is utilizing a time-segmented approach for income planning. By earmarking assets into separate “baskets” with appropriate risk parameters for specific time frames, this strategy helps keep investors less exposed to short-term volatility in the markets as they make withdraws to support income needs. Below is a hypothetical case of how one might implement such a strategy.

Even the most well-informed investors have difficulty in overcoming human impulses that will have us follow the crowd in and out of asset classes, jump to decisions in order to limit perceived losses or succumb to our whims based on the events of the day.

Taking the long-view and sticking to a plan requires placing less emphasis on short-term performance and market fluctuations. We believe the time segmented allocation method offers investors a reliable strategy for meeting their needs.

Time Segmented Allocation

From an investment perspective, the objective of the Nest EGG Analysis and its findings is to present your nest egg in a new format which allows you to make more informed decisions about how much risk you will need to take and how it should be incorporated into a retirement portfolio. When it comes to risk, we believe taking as little as possible while maintaining high confidence that you can meet your retirement goals.

Learn more about the Nest EGG Analysis.

Contact Us:

1650 Borel Place, Suite 227

San Mateo, CA 94402

T-650.573.9960

F-650.573.9930

info@hatchplan.com

![]()

for Bird’s Eye View, our newsletter on longevity issues.

{kind=link}